Global markets have certainly seen their fair share of ups and downs over the course of the year. After a positive first half – albeit led by a select number of stocks – the late summer saw a sharp decline in global equities, leaving investors understandably hesitant about where we go from here. Charlie Buxton, our Head of Investment Management, takes a closer look at recent developments.

The performance from equities and bonds this year has largely been determined by the outlook for interest rates, itself a feature of the stubbornness of inflation – particularly at core level (the cost of goods and services, excluding energy). Negative sentiment has continued to take its toll, with the sharp rise in long-term interest rates weighing heavily on markets.

The US economy is proving more resilient than expected, and oil prices have risen through the course of the year, particularly in the third quarter. These factors are challenging the narrative at the start of this year, which forecast a cooling off in inflation. The reality is that whilst inflation may be growing less quickly, it is not yet at levels that Central Banks are comfortable with.

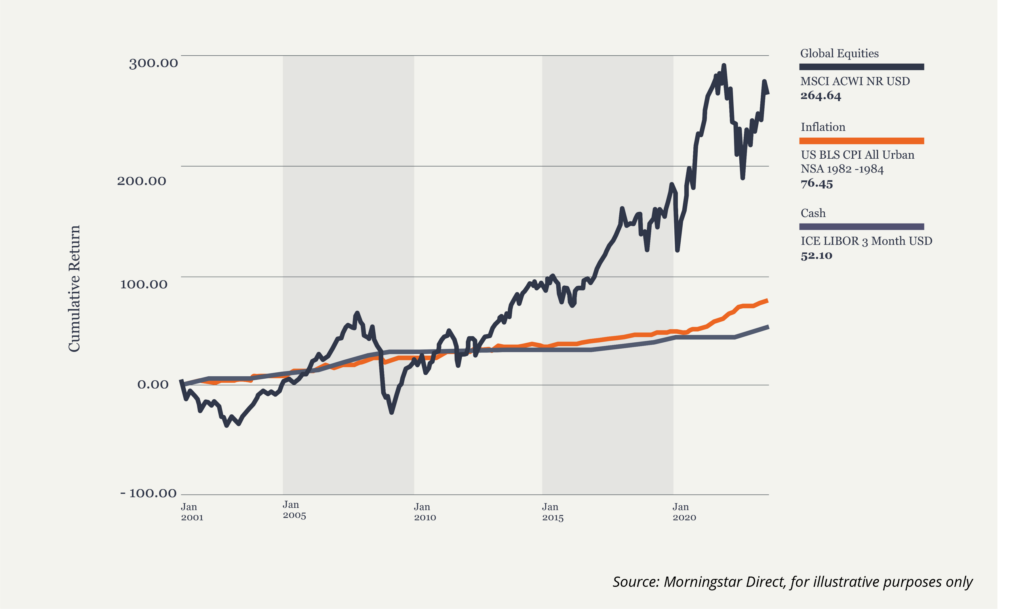

There are also some lingering concerns over China and its post-Covid recovery, despite initial optimism at the start of the year. More recently there’s been a particular focus on its heavily indebted property sector, which has weighed on broader Asia equity markets. Whilst this might prompt investors to look elsewhere or pull back into more liquid assets, it’s worth remembering that equities historically outperform cash over the long-term.

A long-term approach

So where does this leave us? History has shown us time and again, that over the longer term, being committed to an investment strategy that’s suitable for your risk tolerance, remains the best course of action.

Since 2000, global equities have provided a far higher, real (after inflation) return, than cash.

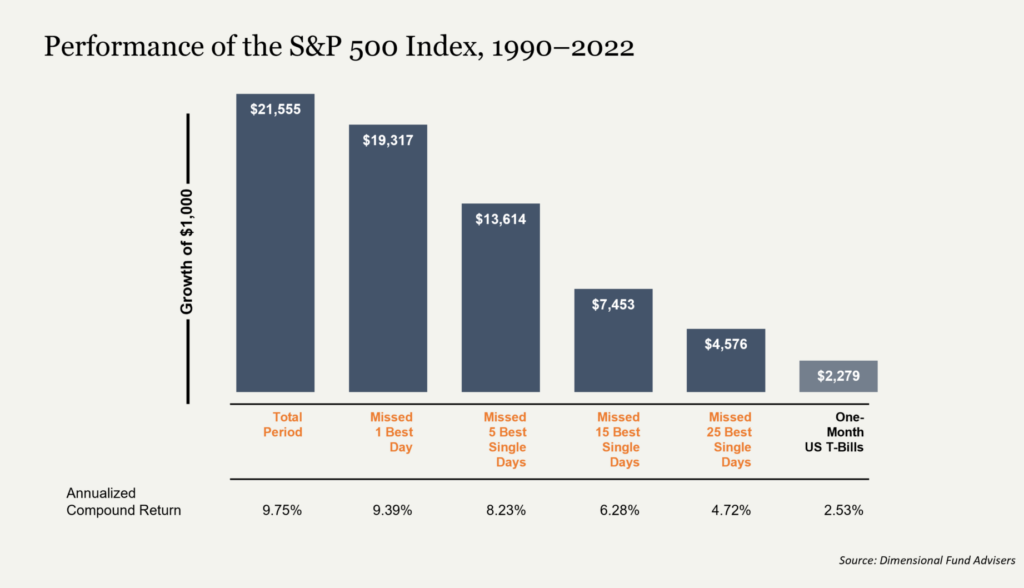

Added to this is the fact that trying to time the market, and pick up on the good returns, whilst avoiding those tricky periods can be costly. The below graphic shows us how being out of the market on the best ten, twenty or thirty days can be detrimental to your portfolio.

So, with all this in mind, our fundamental approach remains the same: investment should be viewed as a long-term activity, with a strategic approach to both asset allocation and fund selection. Investing in global markets is never without some volatility – as we’re currently experiencing – but we know that empirical data supports longer term commitment to equity market investment for long-term capital growth.

Please note that past performance is not necessarily indicative of the future performance.